Secured vs Unsecured Credit Cards for Rebuilding: What It Really Costs

Choosing between a secured card and a subprime unsecured card can cost you hundreds in fees and interest. Here is the simple math, when unsecured ever makes sense, and the fastest rebuild path.

The Setup

You are rebuilding credit. You have two common paths:

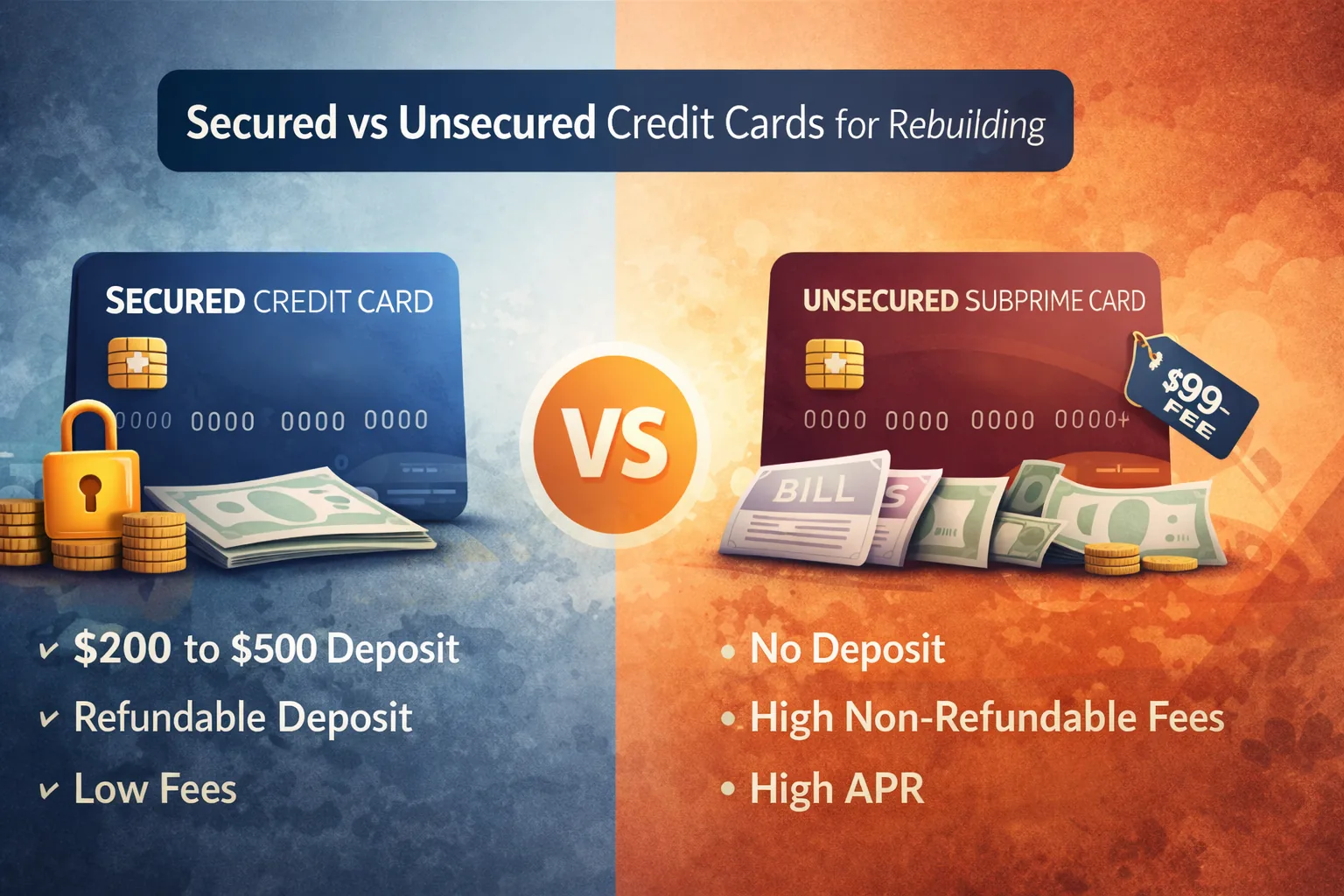

Path A: Get a secured card. Put down $200 to $500. Pay a low annual fee (often $0). Get your deposit back when you close or graduate.

Path B: Get an unsecured subprime card. Pay annual fees. Accept a high APR. Get a low credit limit with part of it sometimes eaten by fees.

The industry acts like these are equivalent options. They are not.

Secured vs Unsecured Cards: The Real Cost Difference

The difference is not vibes. It is math.

A secured deposit is not a fee. It is money temporarily held as collateral.

Most subprime unsecured cards charge fees that are not refundable.

That is the whole game.

The Real Math (With Simple Examples)

Note: card pricing changes. Always confirm current fees and APR on the issuer site before applying.

Secured Card Example (Discover it Secured)

Unsecured Subprime Example (Milestone style card)

Over 12 to 24 months of rebuilding, the typical pattern looks like this:

So the real difference is not $2,000 for everyone.

The real difference is that unsecured subprime can quietly drain a few hundred dollars during the exact season of life when you need cash most.

The Trap People Miss: High APR + Low Limits

Most rebuilders do not plan to carry a balance.

But life happens.

With a high APR and a small limit, one mistake can spiral fast.

Secured cards reduce the odds of that spiral because you are usually starting smaller and treating the card like a credit reporting tool, not a borrowing tool.

When an Unsecured Card Can Make Sense

Honestly, rarely. But there are a few scenarios:

If none of these apply, secured is usually the cleaner move.

The Graduation Myth

Issuers love to talk about graduating from secured to unsecured. Here is what matters:

Pro move: do not wait forever.

After 6 to 12 months of on time payments on your secured card, apply for a better unsecured card. Keep the secured card open for history. Now you have two positive tradelines.

The Credit Union Exception

Credit unions often offer secured cards with:

If you are rebuilding credit, joining a local credit union and getting their secured card can be a strong move.

Bottom Line

The secured vs unsecured debate is not really a debate. It is marketing.

Secured cards are usually cheaper, easier to qualify for, and simpler to use correctly. The only downside is needing money upfront.

If you have $200 to $500 you can tie up for 6 to 12 months, start with a secured card.

If you truly cannot, then consider an unsecured card, but treat fees like the price of admission and keep balances low.

Better is what costs you less and builds credit with fewer mistakes. Usually, that is secured.

Check our reviews to find which secured card offers the best terms for your situation.

FAQ: Secured vs Unsecured Cards for Rebuilding Credit

Is a secured card better than an unsecured card for rebuilding credit

For most people rebuilding, yes. A secured card often has lower fees and is easier to manage safely while you build payment history.

Does a secured card build credit as fast as an unsecured card

Yes. What matters is on time reporting to the bureaus, low utilization, and time. The type of card matters less than how you use it.

Do I get my secured deposit back

Usually, yes, if the account is closed in good standing or you graduate. Always confirm the issuer policy.

Should I carry a balance to rebuild credit

No. Paying in full each month is fine and avoids interest.

Related Card

Annual Fee

$0

APR

28.24% variable

Money Matters Editorial Team

Our editorial team consists of financial experts and credit specialists dedicated to providing honest, data-informed guidance for individuals rebuilding their credit. We review every card based on real-world utility, fee structures, and accessibility for those recovering from financial hardship.